Market Letter - October 2025

FX: The dollar on a rollercoaster, with strong uprising at month-end.

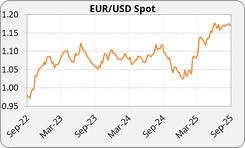

Euro: The euro strengthened against the dollar in mid-September, breaking above the 1.18 level, supported by better-than-expected business sentiment surveys (PMIs) in the euro area. However, it retreated toward 1.17 at the end of the month following the release of solid U.S. second-quarter GDP data at +3.8%, which temporarily boosted the dollar. The greenback’s downward trend resumed in the final days of the month, with EURUSD now trading around 1.174.

US Dollar: The dollar remains volatile, but its downward trend has yet to run its course. The DXY posted a modest monthly decline of around –0.99%, according to historical data. This performance reflects the market’s dilemma: expectations of rate cuts weigh on the dollar, while political uncertainty (shutdown risks, inflation, and Fed communication) prevents a sharper drop, keeping the DXY locked in a consolidation range.

British pound: The pound had a volatile month, pressured by the scale of the U.K.’s public deficit and by a cautious Bank of England that kept its policy rate unchanged at 4%. However, labor market data showing unemployment steady at 4.7% provided some temporary support, with EURGBP ending the month at 0.8742.

Yen: The yen weakened throughout the month against the euro, with EURJPY currently trading around 173.93. The surprise resignation of Prime Minister Ishiba added political uncertainty, while the Bank of Japan maintained its accommodative stance despite persistent domestic inflation. Within the Liberal Democratic Party, several contenders for his succession, such as Takaichi and Koizumi, favor an expansionary fiscal approach, whereas Hayashi is seen as more cautious. A shift toward pro-deficit policies would reinforce expectations of further stimulus and keep downward pressure on the yen.

Yuan: The Chinese yuan saw little movement, with USDCNY holding around 7.11, as the People’s Bank of China kept its benchmark rates unchanged (1-year at 3% and 5-year at 3.5%), which put slight pressure on the currency.

Interest Rates: The Fed begins easing but inflation remains a constraint.

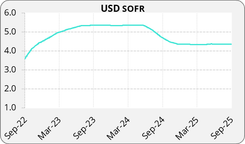

United States: In the United States, the key event was the Federal Reserve’s September 17 decision to cut its policy rate by 25 basis points to 4.00%–4.25%, marking the first reduction since December 2024. Markets still anticipate two additional cuts by the end of 2025, followed by just one in 2026. However, Jerome Powell emphasized at the end of the month that this guidance remains cautious and that further rate cuts are not yet guaranteed.

Markets reacted to the latest inflation data: August CPI came in at 2.9% (vs. 2.7%), PPI at 2.5% (vs. 2.3%), and headline PCE at 2.7% (vs. 2.6%). Core PCE—the Fed’s preferred gauge that excludes food and energy—rose by 2.9% year-on-year (unchanged from July and in line with expectations) and by 0.2% month-on-month. These figures confirm that inflationary pressures remain persistent and above the Fed’s 2% target

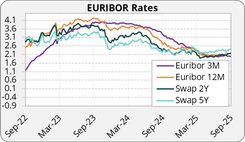

Euro zone: The ECB kept interest rates unchanged for the second consecutive meeting, signaling that its rate-cutting cycle may be over and highlighting risks linked to services inflation and fiscal pressures. Meanwhile, Germany’s Ifo business climate index fell to 87.7, underscoring the fragility of corporate confidence.

United-Kingdom: The Bank of England kept its policy rate at 4%, with a 7–2 vote in favor of maintaining the status quo. This decision highlights the challenge of dealing with inflation still elevated at 3.8% in August, well above the 2% target. Markets, however, are pricing in the possibility of a first cut to around 3.75% by year-end, while closely monitoring upcoming macroeconomic data.

Other regions: The Bank of Japan kept its rates near 0.5% but signaled that a hike could come as early as October if domestic inflation persists.

Commodities: Gold at record high, oil held back by weak demand despite heightened geopolitical risks.

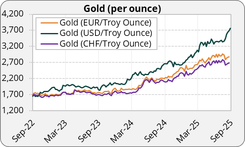

Gold : Gold prices hit a new record above $3,800 on Monday, driven by strong safe-haven demand amid the risk of a U.S. government shutdown and a weaker dollar. Expectations of further Fed rate cuts are also supporting the metal, with markets pricing in around 40 basis points of easing by the end of 2025, a factor that traditionally favors gold during periods of economic or geopolitical uncertainty.

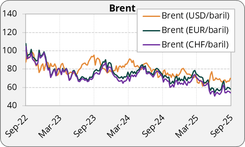

Oil : Brent crude traded between $66 and $68 per barrel, ending the month slightly lower at $67, pressured by weakening global demand, partly offset by stronger European activity data and Chinese strategic buying. Oil prices fell about 2% at the end of September, with Brent down $1.26 to $68.87 after reaching its highest since late July the previous Friday. The decline was mainly driven by expectations of another production increase from OPEC.

Silver and Platinium : Silver and platinum also advanced for similar reasons as gold, supported both by their safe-haven appeal and strong industrial demand. They ended the month at $46 and $1,539 respectively.

Other topics:

U.S. Government Shutdown: What are the impacts? : As the September 30 deadline approaches, the United States faces the risk of a government shutdown, meaning a paralysis of federal services due to the lack of a budget agreement. Such a scenario would likely push gold prices even higher, as it remains the leading safe-haven asset in times of political uncertainty in the U.S. The prospect of a slowdown in U.S. economic activity would weigh on oil demand, potentially driving prices lower despite current supply-side tensions.

In addition, a potential weakening of the U.S. economy could further prompt the Fed to cut rates, which would in turn put additional downward pressure on the dollar against other major currencies.

International Trade / Tariffs: At the end of the month, Donald Trump announced a new wave of tariffs effective October 1, including 100% on certain patented medicines and 25% on heavy trucks and manufactured goods. This decision weighed on European and Asian pharmaceutical stocks and reignited fears of imported inflation.

War in Ukraine: The United States is considering supplying Ukraine with long-range Tomahawk missiles, with Washington’s approval, paving the way for potential deep strikes into Russian territory. Such an escalation would further boost demand for gold as a safe-haven asset and continue to weaken the dollar. This development increases the risk of a wider conflict and fuels a climate of heightened geopolitical volatility in the markets.

This newsletter was written on the 30/09/2025.

OUR TEAM SUPPORTS YOU

Kerius Finance brings together a team of passionate experts dedicated to analyzing, managing, and optimizing financial risks. Our approach is based on transparency, rigor, and attentiveness, enabling us to fully understand your challenges and provide tailored solutions.