Market Letter - December 2025

FX : A month of divergences, with a dollar weakened by delayed US data, European fragilities and heightened yen volatility

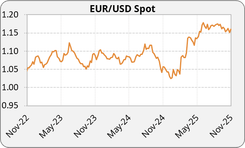

Euro: The euro fluctuated throughout November, caught between a dollar weakened by disappointing U.S. data and a generally softer European backdrop. EURUSD remained volatile but firmed slightly toward the end of the month, returning to around 1.16.US Dollar: The dollar displayed mixed movements over the month, alternating between periods of decline and rebound in response to statements from Donald Trump, who reignited the debate over tariffs. Since early October, the US government shutdown, which led to a partial closure of federal agencies, initially weighed on the currency as markets feared a weakening of economic growth. However, as the situation dragged on, the dollar strengthened, supported by demand for liquid and safe assets, as well as by the Federal Reserve’s decision to cut its key interest rate by 0.25% amid a slowdown in the labor market. Hopes of easing trade tensions with China also helped restore investor confidence and supported the dollar toward the end of the month.

British pound: The pound remained under pressure in October, declining against major currencies following the release of weaker-than-expected inflation data. The headline index held steady at 3.8% in September, while core inflation eased slightly to 3.5%, reinforcing expectations of interest rate cuts by the Bank of England early next year. The EUR/GBP rose to 0.88.

Yen: The yen continued to depreciate against both the euro (177.6 EURJPY) and the dollar (153.5 USDJPY), as the Bank of Japan chose to keep its policy rate unchanged at 0.5% despite persistent inflation hovering around 2.7%. The victory of Sanae Takaichi as leader of the Liberal Democratic Party reinforced expectations of an expansionary fiscal policy and the continuation of the Bank of Japan’s ultra-accommodative monetary stance. Investors anticipate a possible intervention by the Ministry of Finance should the currency breach the 160 USDJPY threshold, but for now, the interest rate differential with the United States continues to exert structural pressure on the yen.

Yuan: The yuan remained stable around 7.11 USDCNY, supported by the signing of the Trump–Xi agreement in Busan, which led to an effective reduction in tariffs on fentanyl-related products (from 20% to 10%) and a one-year postponement of China’s restrictions on rare earth exports. The People’s Bank of China kept its key policy rates unchanged (3% for one year, 3.5% for five years), while its targeted interventions helped limit volatility. A brief spike to 7.14 was nonetheless observed prior to the signing of the agreement, amid the latest round of U.S. tariff threats.

Trade war: Trade tensions intensified this month before easing toward the end of the period with the meeting between Donald Trump and Xi Jinping in Busan. Washington had initially threatened to impose 100% tariffs on Chinese imports but ultimately agreed to halve the duties on fentanyl-related products in exchange for Beijing’s commitment to strengthen controls on precursor chemicals and resume purchases of U.S. soybeans. China also agreed to postpone by one year its new restrictions on rare earth exports, a conciliatory gesture welcomed by the markets. At the same time, the United States raised tariffs by 10% on certain Canadian products, citing unfair competition in the industrial sector, which briefly weighed on North American business confidence before the announcement of the U.S.–China truce.

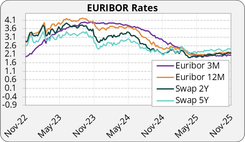

The ECB kept policy unchanged for the third consecutive meeting and is expected to hold rates steady through 2026, while Germany’s industrial downturn deepened (manufacturing PMI at 48.4). Even though the European Commission revised its 2025 growth forecast upward (+1.3% vs. 0.9% previously), the euro failed to gain lasting traction, with investors remaining cautious amid budget uncertainties and persistent pressures in services and food prices.

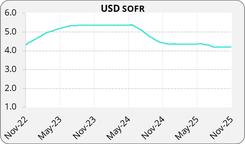

US Dollar: The dollar had an uneven month in November. It was initially supported by a temporary shift toward safe-haven assets and by the absence of data during the long government shutdown, but later weakened as delayed economic indicators were released. Retail sales rose only 0.2%, job losses accelerated, and producer inflation remained moderate (+0.3%). Combined with dovish comments from several Fed officials, these figures significantly strengthened expectations for a December rate cut. Markets now price in nearly an 80% probability of a cut, even as some policymakers argue there is no urgency to ease further given inflation remains above the 2% target.

British pound: The pound showed no clear trend in November, with EURGBP hovering around 0.88 despite a busy UK economic agenda. The presentation of the 2025 Budget by Prime Minister Reeves supported the currency, pushing EURGBP back toward 0.87. Meanwhile, the Office for Budget Responsibility confirmed weaker-than-expected economic conditions and downgraded growth projections. Unemployment increased to 5% and inflation slowed to 3.6%, strengthening expectations of a Bank of England rate cut in December.

Yen: The yen experienced significant volatility against the euro, allowing EURJPY to break above 180 for the first time. This movement mainly reflects continued yen weakness, despite repeated attempts by Japanese authorities to curb its decline.

Throughout the month, senior officials, including advisor Takuji Aida, BoJ Governor Kazuo Ueda, and Finance Minister Satsuki Katayama, reiterated Tokyo’s readiness to intervene if the depreciation threatened economic stability. Thin liquidity periods, particularly around U.S. Thanksgiving, were also seen as potential intervention windows, briefly calming volatility. But these signals were not enough to reverse the trend. The yen remains pressured by October’s large fiscal stimulus package and an ultra-accommodative monetary stance, even as some policymakers begin to contemplate a potential rate hike.

Yuan: The yuan strengthened in November, with USDCNY falling below 7.07, its strongest level in over a year. This move reflects both an improved diplomatic climate, following a call between Donald Trump and Xi Jinping confirming progress on trade and the resumption of bilateral visits from 2026, and stronger support from the People’s Bank of China. The PBoC continued to bolster the currency by setting firmer daily midpoints (around 7.0796, the strongest since October 2024). Seasonal year-end demand, as companies convert dollars to meet obligations, also provided support.

The weaker dollar on growing Fed rate-cut expectations helped as well. Markets now await the Politburo meeting and the Central Economic Work Conference for guidance on 2026 policy priorities.

Interest Rates: General caution, with a divided Fed, a steady ECB and central banks under economic pressure

United States: November marked the end of the shutdown and the return of economic data to guide Fed decisions after October’s uncertainty. Minutes from the latest FOMC meeting showed a deeply divided committee: some members see a December rate cut as necessary to support a cooling labour market, while others argue inflation remains too high to justify easing. Market expectations shifted sharply, with the probability of a 25 bp cut rising from roughly 40% in early November to more than 80% once the government reopened. The delayed September jobs report showed 119,000 job gains, above expectations, but also an uptick in unemployment to 4.4%, the highest since 2021. Other late releases pointed to moderate cooling: producer prices rose 0.3% (driven by energy and food) and retail sales increased just 0.2%, the slowest in four months.

Euro zone: The ECB maintained a cautious stance, leaving rates unchanged for the third consecutive meeting. October HICP inflation came in at 2.1% headline and 2.4% core, close to the 2% target but not low enough to justify a fresh easing cycle.

The ECB still sees the economy supported by a resilient labour market and ongoing fiscal measures, arguing for a prolonged period of stable rates. Markets now expect the first rate cut only from mid-2027 instead of late-2026.

United-Kingdom: The Bank of England kept its policy rate at 4%, but softened its tone amid clear signs of slowing economic activity. Inflation continues to recede, and indicators such as falling consumer confidence, stagnant output, and fiscal pressures fuel expectations of an early rate-cut cycle starting in December. The 2025 Budget added uncertainty, with several measures expected to weigh on households: prolonged income-tax threshold freezes, higher taxation on savings, and changes to salary-sacrifice rules (subject to social contributions above £2,000 per year from 2029). The reform, widely criticised, is likely to reduce retirement-saving incentives.

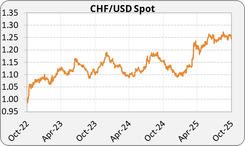

Switzerland: Switzerland’s 0.5% GDP contraction in Q3 was largely driven by the impact of U.S. tariffs, which had been raised to as high as 39% on several Swiss products. The recent reduction to 15% offers some relief for exporters, though the initial shock continues to drag on activity.

Other regions: In Canada, the central bank signalled that rate cuts are unlikely in the near term: headline inflation has eased to 2.2%, while core inflation remains near 3%.

In Australia, the central bank also kept its rate at 3.6%, opting for caution amid still-challenging economic conditions.

Commodities: Gold and metals supported by rate-cut expectations, oil under geopolitical pressure

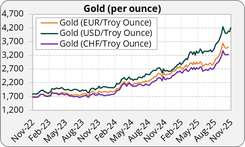

Gold : Gold hovered around $4,150/oz, near a two-week high, supported by delayed U.S. data that fuel expectations of a December Fed rate cut. The metal continues to benefit from a weaker dollar, slower economic momentum, and steady purchases by Asian central banks. Easing tensions between Russia and Ukraine have limited stronger safe-haven inflows.

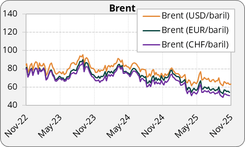

Oil : Brent extended its decline toward $62.5/bbl, reaching a five-week low, weighed down by an already oversupplied market and growing indications of a potential Russia-Ukraine peace agreement. Talks in Geneva were described as “almost finalised” by U.S. President Donald Trump, while Kyiv called them a promising start.

The potential partial lifting of sanctions on Russian crude is adding to oversupply fears at a time when global production continues to exceed consumption.

Near-term volatility remains high, caught between the prospect of Fed easing, supportive for demand, and the risk of additional Russian volumes returning to market. For now, investors are focused on the diplomatic outcome, widely seen as the key driver of year-end pricing.

Silver and Platinium : Silver climbed above $52/oz, hitting a two-week high as expectations of Fed easing increased. Platinum followed suit, rising above $1,570/oz and nearing monthly highs. The metal is supported by prospects of lower rates, constrained global supply, and strong demand from the automotive and hydrogen sectors. Year-to-date, it is up roughly 70%.

Geopolitical Focus: Venezuela enters a new phase of tensions

November saw a significant hardening of the U.S. stance toward Caracas, including the designation of the Cartel de los Soles network as a foreign terrorist organisation and increased U.S. military activity in the Caribbean. Washington accuses the group, linked to senior Maduro-aligned officials, of fuelling drug trafficking, while Cuba denounces an attempted regime-change operation. Despite mounting pressure, Nicolás Maduro shows no intention of stepping down: faced with possible legal action, the military’s dependency on the regime, and the lack of any credible exile option, staying in power appears to be his only viable choice. Oil remains his key bargaining tool. Production, stable around 1.1 million barrels per day, is largely directed to China but could be redirected toward the U.S. or Europe if negotiations progress. U.S. sanctions complicate these potential shifts and add uncertainty: a political breakthrough would increase supply, while military escalation would restrict it. For now, markets favour the scenario of abundant global supply, which continues to weigh on Brent.

This newsletter was written on the 28/11/2025.

OUR TEAM SUPPORTS YOU

Kerius Finance brings together a team of passionate experts dedicated to analyzing, managing, and optimizing financial risks. Our approach is based on transparency, rigor, and attentiveness, enabling us to fully understand your challenges and provide tailored solutions.