Market Letter - February 2026

FX: dollar under pressure, volatility on the rise

EURUSD: In January, EURUSD was the key pair of the month: the euro broke above 1.20 (for the first time since mid-2021) and ended the period around 1.191. The main driver was not a “Europe surprise” but a weaker dollar: markets priced in a higher risk premium linked to US economic policy (trade tensions) and repeated criticism of the Fed, weighing broadly on the USD. In contrast, the euro area stayed on a readable track (ECB in status quo, inflation around 2%), which reinforced the divergence.

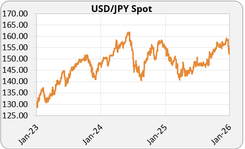

USDJPY: The yen is also a currency to watch. After the dollar peaked around 159.23, the pair fell to 153.81 (the yen’s strongest level in four months) after market signals were interpreted as a warning and as a lower threshold for potential intervention. The yen then fluctuated with recurring rumors of coordinated intervention to stabilize the currency rumors that were mostly denied.

EURJPY: The yen’s structural weakness was even more visible against the euro: EURJPY set a record at 186.64 in January, driven by rate differentials and recurring concerns around Japan’s fiscal trajectory. The cross then remained highly sensitive to the same drivers as USDJPY.

EURCHF: The CHF fully played its safe-haven role. EURCHF slipped toward the 0.92 area, with a low around 0.915, returning to levels seen during the most acute stress episodes since 2015. The move mainly reflects safe-haven demand for CHF in a tense geopolitical backdrop, keeping the pair highly sensitive to any signals from the SNB.

Interest rates: central banks on hold, markets under strain

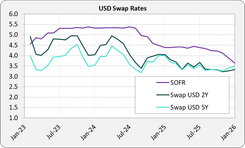

United States: The Fed’s January meeting confirmed a clearly wait-and-see stance. The FOMC kept the policy rate unchanged at 3.50–3.75%, highlighting an economy that remains “solid,” a labor market that is cooling, and inflation that is still elevated. Jerome Powell reiterated there is no urgency to resume rate cuts: disinflation is progressing, but the Fed wants more evidence before acting. He also noted that policy has already been eased by 75 bps since September, and that the path ahead will remain strictly data-dependent, with close attention to potential inflation effects from tariffs.

Euro zone: In the euro area, the ECB kept a clear direction: status quo. The December accounts show the Governing Council is not preparing markets for a rapid cut and remains comfortable with unchanged rates (deposit 2.00%, refi 2.15%, marginal lending 2.40%). Inflation back to 2.0% in December supports that scenario. Toward month-end, several officials also pointed out that an overly strong euro driven by a weaker dollar could pull inflation lower and influence upcoming decisions.

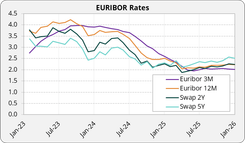

United Kingdom: The BoE remains in “slow and cautious cuts” mode after December’s reduction, with the policy rate at 3.75%. In January, UK inflation surprised to the upside (CPI 3.4% in December, services 4.5%), and internal messaging refocused on wage risks, limiting the case for back-to-back cuts. The 5 February meeting is expected to be a hold, and a cut in March is the base case, but far from certain.

Japan: In January, the BoJ kept its policy rate unchanged at 0.75% and raised its growth/inflation projections, without signaling an imminent move. The key development was the rise in long-dated yields: JGBs sold off as markets priced a higher fiscal risk ahead of the election (tax-cut/spending promises), pushing the 10-year toward 2.15% (a 27-year high) and the long end to record levels (20-year 3.135%, 30-year 3.52%). Ueda was clear on the framework: the next step will depend on wages and the breadth of inflation, while closely monitoring “excessive” moves in the curve; a weak yen and a tight labor market remain factors that could bring the next hike forward.

Commodities: a rush into precious metals amid uncertainty

Oil: The month started without a clear trend, then accelerated sharply into month-end as a geopolitical premium returned. Brent was trading around $70/bbl (WTI $66/bbl), supported by rising US-Iran tensions and, in the background, more tactical factors (lower US inventories, weather-related disruptions to production). Venezuela remained a closely watched theme, but its impact on prices was mostly gradual: headlines shaped sentiment, while the effect on volumes is likely to play out over time.

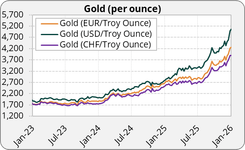

Gold: January marked a rush into safe-haven assets. Spot gold reached a peak of $5,500/oz before falling about 7% into month-end to trade around $5,000/oz. The move reflects demand for protection amid geopolitical tensions, a weaker dollar, and sustained demand (central bank buying and investment flows).

Silver: Silver amplified gold’s safe-haven move, with a much more volatile rally driven by hedging demand and strong momentum: after a high around $120/oz, it was trading around $100/oz at month-end.

Copper: At the same time, copper advanced on a mix of “real assets” positioning and supply concerns: LME 3-month copper was trading around $13,150/t, leaving the market highly sensitive to Chinese demand and any supply-side surprises.

This newsletter was written on the 01/30/2026.

OUR TEAM SUPPORTS YOU

Kerius Finance brings together a team of passionate experts dedicated to analyzing, managing, and optimizing financial risks. Our approach is based on transparency, rigor, and attentiveness, enabling us to fully understand your challenges and provide tailored solutions.