Market Letter - January 2026

FX : Currencies adjusting to the pace of central bank policy cycles

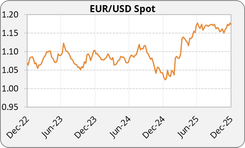

EURUSD: December confirmed a structural weakening of the US dollar, following the Federal Reserve’s rate cuts and growing expectations of a monetary pause in early 2026. Against this backdrop, the euro appreciated steadily, moving back above 1.16 in the first week of the month and reaching the 1.18 area by month-end, its highest level since autumn.

The euro was also supported by the European Central Bank’s prudent yet firm stance. The ECB kept rates unchanged in December, with the main refinancing rate at 2.15% and the deposit rate at 2.0%. Christine Lagarde reiterated the absence of any pre-defined rate path and stressed a strictly data-dependent approach in a context of heightened uncertainty.

EURGBP: Against the pound sterling, EURGBP remained elevated, trading in a 0.87-0.88 range throughout the month. Sterling was weighed down by a stagnating economy and a weakening labor market, despite the Bank of England’s decision to cut its policy rate by 25 basis points to 3.75%, its lowest level since 2022. This was the first rate cut since August and was decided by a narrower margin than expected, with five committee members voting in favor of the cut and four opting for no change. This less dovish outcome prompted markets to scale back expectations of further near-term rate cuts.

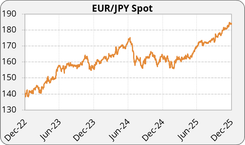

EURJPY: In Asia, EURJPY traded between 181 and 182 over the course of the month. The yen remained under pressure early on before strengthening following the Bank of Japan’s decision to raise its policy rate by 25 basis points to 0.75%, the highest level since 1995. This widely anticipated move confirms the continuation of a gradual monetary normalization process in Japan.

Interest Rates: Between US easing and European status quo

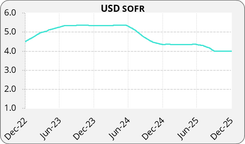

United States: The Federal Reserve cut its policy rate to a 3.5-3.75% range, its lowest level since 2022, while signaling a likely pause in early 2026 to assess economic developments. This decision contributed to looser financial conditions and the broad-based weakening of the US dollar observed over the month.

However, macroeconomic data released toward month-end painted a more nuanced picture. US GDP grew at an annualized rate of 4.3% in the third quarter of 2025, its strongest pace in two years, up from 3.8% in the previous quarter and above market expectations. This acceleration was mainly driven by strong household consumption, rising exports, and a larger contribution from public spending.

Labor market data also showed signs of stabilization. Job creation reached 64,000 in November, following a decline of 105,000 in October and exceeding market expectations. Hiring was concentrated in healthcare and construction, while federal employment continued to decline. Overall, these indicators underline the resilience of the US economy and could lead the Fed to adopt a more cautious approach to the pace of rate cuts in 2026.

United-Kingdom: The Bank of England’s rate cut took place against a backdrop of easing inflation and increasing strain on economic activity. The Monetary Policy Committee emphasized that future adjustments would remain closely tied to the inflation outlook, while acknowledging that the restrictive stance of monetary policy has already begun to ease. This communication led markets to moderate expectations of rapid further rate cuts.

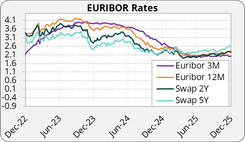

Euro zone: The ECB’s decision to keep rates unchanged reflects persistently uneven inflation dynamics across countries and elevated economic uncertainty. After a sharp rise in rates earlier in the month, markets subsequently stabilized, with the 5-year Euribor 3-month swap rate hovering around 2.50%. Nevertheless, the probability of a rate hike in 2026 remains significant.

Japan: Annual inflation eased slightly to 2.9% in November, mainly due to lower food price inflation, while remaining above the central bank’s target. The Bank of Japan expects wage growth to continue in 2026, supported by improving corporate profits, reinforcing the case for the ongoing normalization of monetary policy.

Commodities: Oil in decline, rising geopolitical risk in Venezuela

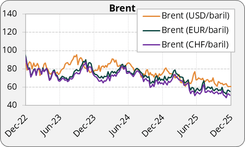

Oil : Oil prices declined sharply over the month, with Brent falling from the $63 area to below $60 per barrel, a multi-year low. This drop reflects rising expectations of a supply surplus in 2026, driven by higher global production, the return of Iraqi volumes, and growing floating storage, particularly of Russian and Iranian crude. Hopes of geopolitical de-escalation between Russia and Ukraine also contributed to a reduction in risk premia. However, late December and early January saw a rise in geopolitical uncertainty following a US-led operation in Venezuela, which resulted in the arrest of President Nicolás Maduro in early January 2026. While the immediate impact on oil flows has remained limited, given Venezuela’s already constrained export capacity, the event has revived geopolitical risk premia and contributed to increased volatility in energy markets, without altering the medium-term oversupply narrative.

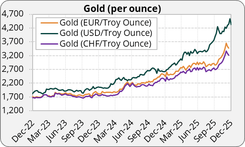

Gold : Gold initially benefited from falling US interest rates, briefly moving above $4,200 per ounce, before stabilizing around $4,300 toward month-end as investors took profits.

Silver and Copper: Silver followed a similar trajectory after reaching record highs. Copper declined toward the end of the month, weighed down by uncertainty over Chinese demand, despite ongoing constraints on global supply.

This newsletter was written on the 05/01/2026.

OUR TEAM SUPPORTS YOU

Kerius Finance brings together a team of passionate experts dedicated to analyzing, managing, and optimizing financial risks. Our approach is based on transparency, rigor, and attentiveness, enabling us to fully understand your challenges and provide tailored solutions.