Market Letter - November 2025

FX : The dollar strengthens following the Fed and ECB announcements

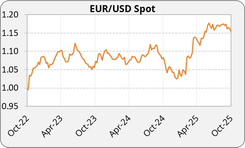

Euro: The euro emerged as the main loser of the month. After a brief rebound at the start of October, the European currency resumed its downward trend against the dollar, falling below the $1.16 threshold, its lowest level in two months. This decline can be attributed mainly to two factors. First, the political shock in France, marked by the unexpected resignation of Prime Minister Sébastien Lecornu and the reshuffling of President Macron’s government, led to a widening of the sovereign risk premium. Second, the European Central Bank’s cautious stance, keeping interest rates unchanged for the third consecutive time, weighed on the single currency. The institution noted that the European economy “continued to grow despite the challenging global environment,” supported by a “robust” labor market, solid corporate balance sheets, and the lagged effects of past monetary easing. In this context of reduced political and fiscal visibility, investors chose to scale back their long positions on the euro.

US Dollar: The dollar displayed mixed movements over the month, alternating between periods of decline and rebound in response to statements from Donald Trump, who reignited the debate over tariffs. Since early October, the US government shutdown, which led to a partial closure of federal agencies, initially weighed on the currency as markets feared a weakening of economic growth. However, as the situation dragged on, the dollar strengthened, supported by demand for liquid and safe assets, as well as by the Federal Reserve’s decision to cut its key interest rate by 0.25% amid a slowdown in the labor market. Hopes of easing trade tensions with China also helped restore investor confidence and supported the dollar toward the end of the month.

British pound: The pound remained under pressure in October, declining against major currencies following the release of weaker-than-expected inflation data. The headline index held steady at 3.8% in September, while core inflation eased slightly to 3.5%, reinforcing expectations of interest rate cuts by the Bank of England early next year. The EUR/GBP rose to 0.88.

Yen: The yen continued to depreciate against both the euro (177.6 EURJPY) and the dollar (153.5 USDJPY), as the Bank of Japan chose to keep its policy rate unchanged at 0.5% despite persistent inflation hovering around 2.7%. The victory of Sanae Takaichi as leader of the Liberal Democratic Party reinforced expectations of an expansionary fiscal policy and the continuation of the Bank of Japan’s ultra-accommodative monetary stance. Investors anticipate a possible intervention by the Ministry of Finance should the currency breach the 160 USDJPY threshold, but for now, the interest rate differential with the United States continues to exert structural pressure on the yen.

Yuan: The yuan remained stable around 7.11 USDCNY, supported by the signing of the Trump–Xi agreement in Busan, which led to an effective reduction in tariffs on fentanyl-related products (from 20% to 10%) and a one-year postponement of China’s restrictions on rare earth exports. The People’s Bank of China kept its key policy rates unchanged (3% for one year, 3.5% for five years), while its targeted interventions helped limit volatility. A brief spike to 7.14 was nonetheless observed prior to the signing of the agreement, amid the latest round of U.S. tariff threats.

Trade war: Trade tensions intensified this month before easing toward the end of the period with the meeting between Donald Trump and Xi Jinping in Busan. Washington had initially threatened to impose 100% tariffs on Chinese imports but ultimately agreed to halve the duties on fentanyl-related products in exchange for Beijing’s commitment to strengthen controls on precursor chemicals and resume purchases of U.S. soybeans. China also agreed to postpone by one year its new restrictions on rare earth exports, a conciliatory gesture welcomed by the markets. At the same time, the United States raised tariffs by 10% on certain Canadian products, citing unfair competition in the industrial sector, which briefly weighed on North American business confidence before the announcement of the U.S.–China truce.

Interest Rates: The Fed cuts rates while the ECB keeps its policy unchanged

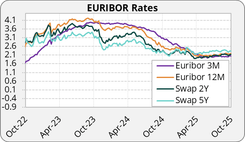

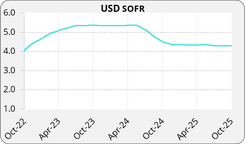

United States: U.S. rates fell sharply over the period. The five-year swap rate dropped to 3.17%, down about 20 basis points since early October. This movement reflects expectations of further Federal Reserve rate cuts amid signs of economic slowdown.

Concerns remain elevated regarding the regional banking sector, weakened by losses linked to alleged fraud cases and the depreciation of bond portfolios. The prolonged government shutdown, which has deprived the Fed of several key macroeconomic indicators, has also weighed on confidence. The Federal Reserve lowered its policy rate by 25 basis points to 3.75–4.00%. It also announced the end of balance sheet reduction as of December 1, in order to preserve liquidity and support financing conditions. However, Jerome Powell emphasized the Committee’s cautious stance, noting that this could be the final rate cut of 2025 given internal divergences.

Euro zone: The ECB kept its rates unchanged for the third consecutive meeting, confirming a cautious approach amid moderate growth. The deposit rate remains at 2%, and President Christine Lagarde stated that the central bank is now in a “good position,” with inflation moving closer to target. The 5-year 3M Euribor swap rate declined from 2.32% to 2.18%. European bond markets remain highly sensitive to political risk, particularly in France, where the OAT–Bund spread reached a ten-month high of nearly 85 basis points.

United-Kingdom: Core inflation in the UK edged down in September 2025 to 3.5%, compared with 3.6% the previous month. This figure came in below market expectations of 3.7% and marks the lowest level since May. Money markets do not anticipate any major changes at the November 6 meeting, with the implied rate standing at 3.90%, suggesting only a limited probability of a cut. In contrast, the December 18 meeting is seen as the expected starting point for a clearer easing cycle, with around 65 basis points of rate reductions priced in by investors by the end of the year.

Other regions: The Bank of Japan is keeping its rates near 0.5%, but the market has begun to anticipate a partial normalization of monetary policy in early 2026 if inflation remains above 2%.

Commodities: Oil fluctuates amid oversupply concerns and renewed sanctions on Russia

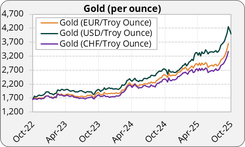

Gold : Gold experienced a spectacular surge in October, reaching an all-time high of $4,381/oz before sharply correcting, marking its steepest one-day drop since 2020 (–6%). This rally, driven by a weaker dollar, lower interest rates, and record central bank demand (notably from China and Turkey), was interrupted by profit-taking in an increasingly overbought market. The correction was amplified by the dollar’s rebound, a slight easing of U.S.–China tensions, and a decline in physical demand. Markets still expect a Fed rate cut in December (with a 60% probability), a structurally supportive factor for gold.

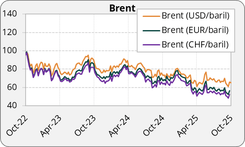

Oil : Brent crude experienced a volatile October, briefly falling below $62/barrel before closing around $66, following U.S. sanctions on Rosneft and Lukoil, two of Russia’s largest producers, accounting for roughly half of the country’s output. This decline was driven by the gradual increase in OPEC+ production, the continued weakness in Asian demand, particularly in China, where imports fell 8% year-on-year, as well as by the IEA’s forecasts of an oil supply surplus for 2026. Toward the end of the month, however, prices recovered, supported by renewed geopolitical tensions in the Middle East, which reignited fears of supply disruptions.

Silver and Platinium : Silver followed gold’s trend, retreating toward $48/oz amid renewed optimism over U.S.–China trade negotiations, yet maintaining its status as a precious and safe-haven metal. Platinum rebounded to around $1,622/oz, supported by strong industrial demand, particularly from the automotive and hydrogen sectors, as well as by supply constraints in South Africa.

Focus Japan:

Japan is experiencing a historic moment: the Nikkei 225 has just surpassed 52,000 points for the first time, symbolizing the powerful comeback of an economy long considered sluggish. Since April, the index has surged by 65%, driven by a combination of fiscal stimulus, structural reforms, and a persistently weak yen. Newly in office, Prime Minister Sanae Takaichi made a bold move with a ¥13.9 trillion stimulus package focused on infrastructure and fiscal expansion. Her strategy rests on a winning combination: proactive fiscal policy and accommodative monetary conditions. The results are visible, wages are rising, companies are reinvesting, and foreign investors are pouring in.What are the impacts? : As the September 30 deadline approaches, the United States faces the risk of a government shutdown, meaning a paralysis of federal services due to the lack of a budget agreement. Such a scenario would likely push gold prices even higher, as it remains the leading safe-haven asset in times of political uncertainty in the U.S. The prospect of a slowdown in U.S. economic activity would weigh on oil demand, potentially driving prices lower despite current supply-side tensions.

Yet a growing concern looms in the background: the potential drift of public debt. With debt levels close to 260% of GDP, Japan remains the most heavily indebted country in the developed world, an equilibrium long made sustainable by near-zero interest rates, strong domestic savings, and an omnipresent Bank of Japan in the bond market.

However, the context is shifting. Inflation has returned, the Bank of Japan has already raised its policy rate to 0.5%, and the massive stimulus programs launched by Sanae Takaichi are increasing public financing needs. Should long-term rates rise, the debt burden could quickly become overwhelming. At the end of the month, Donald Trump announced a new wave of tariffs effective October 1, including 100% on certain patented medicines and 25% on heavy trucks and manufactured goods. This decision weighed on European and Asian pharmaceutical stocks and reignited fears of imported inflation.

In such a scenario, the Japanese currency would be the first casualty. A depreciation beyond 160 or even 170 yen per dollar would become plausible, boosting exports, but eroding domestic purchasing power. The United States is considering supplying Ukraine with long-range Tomahawk missiles, with Washington’s approval, paving the way for potential deep strikes into Russian territory. Such an escalation would further boost demand for gold as a safe-haven asset and continue to weaken the dollar. This development increases the risk of a wider conflict and fuels a climate of heightened geopolitical volatility in the markets.

The repercussions would not stop at Japan’s borders. The country holds more than $1 trillion in U.S. Treasuries. In the event of a domestic crisis, Tokyo might be forced to sell large portions of its foreign assets to support the yen or refinance its debt, triggering a sharp rise in U.S. yields and a shockwave across global markets. A plunging yen would also strengthen the dollar, hurting U.S. exports and adding pressure on emerging economies burdened with dollar-denominated debt.

In other words, if Japan were to derail, it would not merely face a national crisis, but a potential systemic global risk. In an environment already saturated with public debt and constrained monetary policies, the sustainability of Japan’s model has become an early barometer of global financial stability.

This newsletter was written on the 31/10/2025.

OUR TEAM SUPPORTS YOU

Kerius Finance brings together a team of passionate experts dedicated to analyzing, managing, and optimizing financial risks. Our approach is based on transparency, rigor, and attentiveness, enabling us to fully understand your challenges and provide tailored solutions.