Probability of the EURIBOR returning to positive territory

Given the current market volatility, what is the probability that Euribor will rise above 0% or 1% in the coming years?

SUMMARY OF THE ANALYSIS

The analysis below answers this question from a probabilistic perspective, using several methodologies. However, it is important to keep in mind that these methods have a major limitation: they rely on past volatility to infer future movements. As shown by the calculations, the choice of historical assumptions has a strong impact on the results.

Moreover, past performance is never a guarantee of future outcomes, especially during periods of crisis. The COVID-19 crisis made all previous statistical analyses obsolete. As a result, these methodologies are poor decision-making tools when it comes to implementing hedging strategies.

From a risk-management perspective, it is recommended to protect financing costs against Euribor scenarios, even those with a very low probability, as such scenarios could create liquidity issues.

In addition, since financing agreements generally include a 0% floor on Euribor, borrowers face a strong asymmetry of risk: potential losses in the event of rising rates are much greater than potential gains in the event of further declines. This is because the cost of debt hedging with a floor is currently very low and cannot become negative, even if Euribor falls further.

DETAILED ANALYSES

Historical volatility method – EUR 3M

Over the last three months, Euribor 3M fixings have been stable, ranging between -0.5560% and -0.5240%, with an average of -0.5418%. Volatility during this period was extremely low, with a standard deviation of 0.0465%. Using this historical volatility approach, the probability of Euribor rising above 0% in the short term is statistically negligible (<0.0001%).

Over the last 12 months, Euribor fixings remained relatively stable, with a noticeable spike in March 2020. During this period, the index ranged between -0.5560% and -0.16%, with an average of -0.45%. The daily standard deviation was 0.0979%, corresponding to an annualized volatility of 1.55%. Based on this method, the probability of Euribor rising above 0% in the short term becomes significant (around 40%).

Historical volatility of projected EUR 3M rates

Over the last three months, Euribor 3M fixings have been stable, ranging between -0.5560% and -0.5240%, with an average of -0.5418%. Volatility during this period was extremely low, with a standard deviation of 0.0465%. Using this historical volatility approach, the probability of Euribor rising above 0% in the short term is statistically negligible (<0.0001%).

Over the last 12 months, Euribor fixings remained relatively stable, with a noticeable spike in March 2020. During this period, the index ranged between -0.5560% and -0.16%, with an average of -0.45%. The daily standard deviation was 0.0979%, corresponding to an annualized volatility of 1.55%. Based on this method, the probability of Euribor rising above 0% in the short term becomes significant (around 40%).

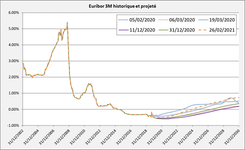

Historical volatility of projected EUR 3M rates

The curve shown above consists of a historical section and a projected section based on market expectations observed at different dates. These projections constantly evolve in response to changes in market expectations, central bank actions and communications, inflation forecasts, and growth outlooks.

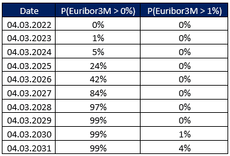

By analyzing the volatility of 15 projected yield curves over the past 15 months, it is possible to estimate the theoretical probability that Euribor 3M will exceed certain thresholds (0% and 1%) at a given date.

Assuming that projected Euribor 3M levels follow a normal distribution, the expected value and volatility of these projections lead to the following conclusions:

- The probability of Euribor 3M rising above 0% becomes statistically significant in 2025 and high from 2026 onward.

- The probability of Euribor 3M rising above 1% before 2030 is statistically negligible.

THE LIMITATIONS OF STATISTICAL MODELS: THE BLACK SWAN

These statistical analyses rely heavily on historical volatility to estimate future movements. As illustrated, the choice of historical data dramatically alters the conclusions.

Furthermore, any major health, economic, or financial shock can quickly render historical data — and therefore the conclusions drawn from them — obsolete.

For example, the sharp Euribor movements in early 2020 could not have been detected by any statistical model based on recent historical data. This highlights the importance of not relying blindly on statistical models and maintaining a pragmatic approach to risk management.

Reminder on risk asymmetry for borrowers

Financing structures that include a 0% Euribor floor create a strong asymmetry of risk for borrowers. They do not benefit from further rate declines but can incur significant losses if rates rise. This asymmetry argues in favor of increased hedging, particularly in volatile environments, especially since hedging costs remain historically low.

OUR TEAM SUPPORTS YOU

Kerius Finance brings together a team of passionate experts dedicated to analyzing, managing, and optimizing financial risks. Our approach is based on transparency, rigor, and attentiveness, enabling us to fully understand your challenges and provide tailored solutions.